As of early October, 2025: A Shift from Policy Fog to Structural Concern

The financial world has moved through a major inflection point. After an uncertain economic policy outlook dominated the first half of the year, the third quarter brought more clarity. The US tariff regime appears largely set, fiscal policy was solidified by the “One Big Beautiful Bill Act,” and the Federal Open Market Committee (FOMC) delivered an anticipated rate cut in September.

Financial markets have responded to this reduction in immediate policy risk with a period of relatively low volatility, a cyclical calm that is expected to persist for the next few months. However, underneath this placid surface, a new set of longer-term, structural fragilities are growing, shifting investor focus from day-to-day policy headlines to deep-seated systemic risks.

1. The Commodity Story: Metals Validate Structural Anxiety

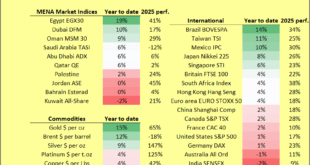

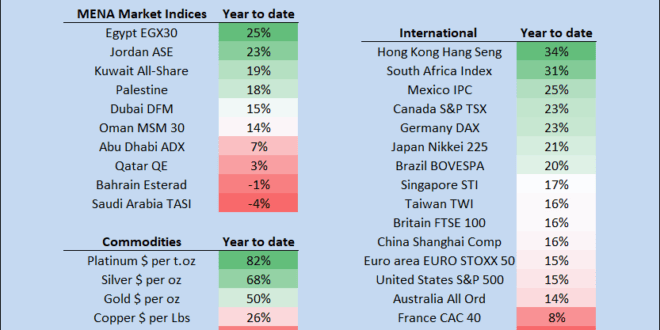

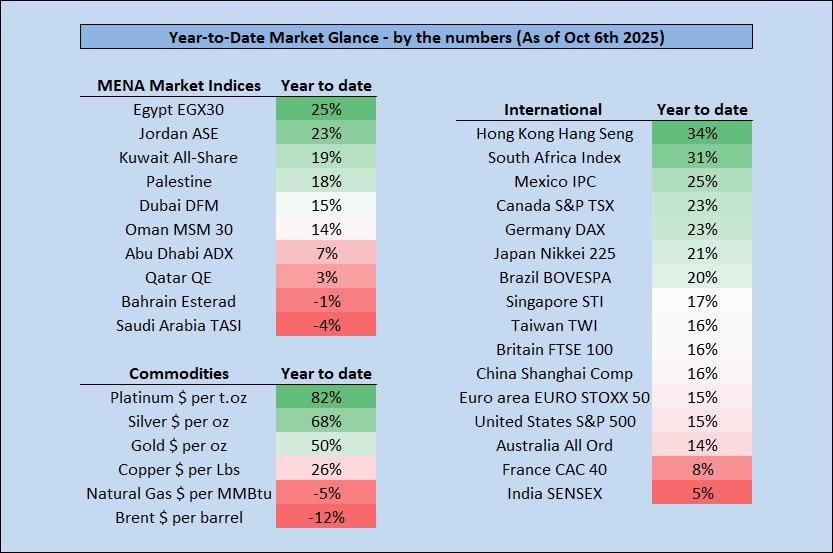

The Year-to-Date (YTD) performance remains dominated by the incredible rally in metals, which now appears to be a vote of no-confidence in the structural stability of fiat currency and developed-world fiscal health:

Platinum has delivered an astonishing 82% YTD return, leading all major asset classes.

Silver (up 68%) and Gold (up 50%) have also posted phenomenal gains. This safe-haven trend is widely expected to continue, with some major research houses raising Gold price targets to the to $4,200/oz range through mid-2026, driven by continued central bank demand and a weak US Dollar outlook.

In contrast, Brent crude oil is down -12% per barrel YTD, and Natural Gas has fallen by -5%, potentially signaling subdued industrial demand or stabilized supply.

2. Global Equities: Outperformance Outside the G7

Despite the mid-year policy turmoil, select international and emerging markets have delivered powerful YTD returns, benefiting from regional dynamics and specific commodity exposure:

Hong Kong’s Hang Seng index leads the global indices, surging 34% YTD.

The South Africa Index has returned 31%, heavily supported by its exposure to the metals and mining complex.

Mexico’s IPC is up 25%, signaling robust activity in North American trade.

The United States S&P 500 (15%) and major developed indices like the Germany DAX (23%) and Japan Nikkei 225 (21%) have delivered solid returns.

MENA Regional Snapshots

The Middle East and North Africa (MENA) region continues to show strong, but divergent, performance:

Egypt’s EGX30 leads the MENA region with a powerful 25% gain.

Jordan’s ASE is up 23% YTD.

Saudi Arabia’s TASI is down -4%, and Bahrain Esterad is down -1%, reflecting internal pressures, a cautious energy outlook, and regional consolidation.

3. Q4 Outlook: The Pivot to Structural Fragilities & AI Concentration Risk

As we close out 2025, the key challenge for investors is distinguishing between cyclical calm and structural risk. The most pronounced risk remains the narrow foundation of the US equity market:

The Concentrated US Bull Market: Despite the S&P 500’s solid return, the US bull run is widely characterized as a “one-note narrative” driven almost entirely by the generative AI (GenAI) capital expenditure boom. The AI data center-ecosystem stocks (the Magnificent Seven and surrounding companies) have accounted for roughly 75% of the S&P 500’s returns and 80% of its earnings growth since the end of 2022. This extreme concentration, coupled with negative free-cash-flow growth for some hyperscalers, suggests the AI-fueled market may be closer to the “seventh inning than the first” of the boom, indicating a high risk of a late-cycle, speculative rally that is vulnerable to corrections.

Structural Fragilities:

Fiscal Vulnerabilities: There is growing concern about fiscal vulnerabilities throughout the developed world. The towering debt levels will increasingly drive long-term yield demands and currency volatility.

The Dollar’s Role: Questions persist about the role of the dollar as the undisputed global reserve currency. This doubt directly fuels the rally in gold and silver, as investors seek alternative stores of value.

Central Bank Independence: The threat to central bank independence in the US is an issue with potentially massive long-term implications for inflation and capital allocation.

In short, the extraordinary YTD returns in safe-haven assets and regional equities have been a leading indicator of these deep structural concerns. The key to navigating Q4 will be recognizing that the diminished short-term volatility is masking profound, increasing structural risks.