The past two months have witnessed a notable turnaround in many market indices, with several even erasing earlier losses. As we hit the mid-year mark, the overall picture reveals a strong performance across many MENA and International markets, while commodities, particularly precious metals, have been standout performers.

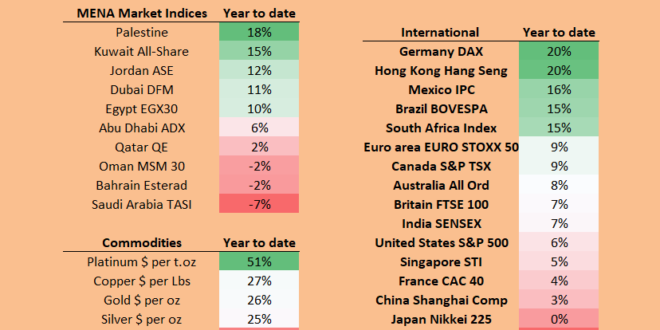

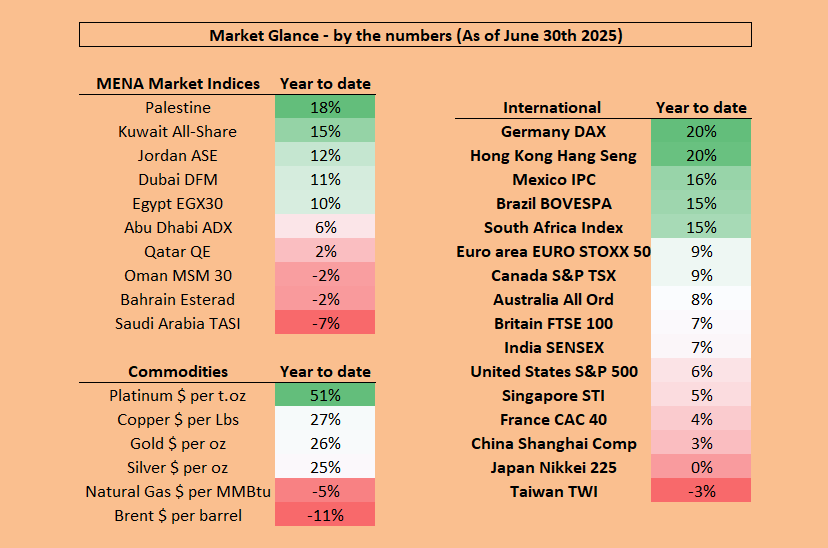

MENA Market Indices: Not What It Looks

The MENA region experienced a significant positive shift over the last two months. Palestine, which was previously down, has surged to an impressive 18% year-to-date gain. Similarly, Kuwait All-Share saw its gain climb to 15%. Jordan ASE also showed strong momentum, moving to 12%.

However, it’s crucial for investors to understand that this performance in the Al-Quds Index may not accurately reflect the underlying fundamentals of the broader Palestinian economy. The index is heavily concentrated, with just three companies—Palestine Telecommunications (PALTEL), Bank of Palestine (BOP), and PADICO (Palestine Development & Investment Company)—making up approximately 69% of its total weight. This means that the index’s component values typically see notable shifts, during periods of dividend payments from these major constituents, which doesn’t reflect fundamentals. From a fundamental viewpoint, the Palestinian economy faces persistent economic hardship, and uncertainty. This environment is characterized by widespread destruction of infrastructure and severe restrictions on movement and trade, contributing to high unemployment and significant contractions in various key sectors.

While most MENA indices recovered, a notable exception was Saudi Arabia TASI, which remains in negative territory of -7% in 2025. The decline in the Saudi stock market has been influenced by underperformance in key sectors and significant heavyweight stocks. Notably, the Utilities and Media sectors have experienced substantial downturns, acting as a drag on the overall index. Additionally, the poor performance of major stocks, such as Acwa Power, has also contributed to the market’s decline.

International Markets: Broad-Based Gains and a US Rebound

The international landscape also painted a much brighter picture by mid-year. Germany DAX and Hong Kong Hang Seng have truly excelled, with year-to-date gains of over 20%.

One of the most significant shifts has been in the United States S&P 500, which dramatically recovered from a steep double-digit loss to a positive 6% year-to-date. This indicates a strong rebound in US equities over the past two months.

Whilst, there remain notable stock markets due to their economies, like Japan’s Nikkei 225 remains barely positive at 0%, and Taiwan’s TWI still in the red at -3%.

Commodities: Platinum Leads the Charge, Energy Remains Volatile

Commodities have continued to deliver impressive returns, with some truly exceptional performances. Platinum has surged to an incredible 51% year-to-date gain, making it the top performer across all categories. This was due to both a diminishing supply and robust demand. Above-ground inventories of platinum are rapidly depleting, and the market faces structural supply constraints, notably due to production challenges in South Africa, a major global supplier. While simultaneously, demand for platinum is robust and growing across several key sectors like the automotive industry.

Gold also maintained its strong momentum, with a year-to-date gain of 26%, while Silver followed suit at 25%. Copper also showed robust growth, now at 27%.

In the energy sector, Natural Gas has seen some recovery but remains negative at -5%. Brent crude oil, however, extended its losses, now at -11% by the end of June, indicating continued headwinds for oil prices.

H2 2025 Financial Market Outlook: Positioning for Opportunity Amid USD Weakness

As we enter the second half of 2025, the market environment remains constructive but selectively volatile. A projected US soft landing, broad-based policy easing, and a structurally weakening dollar form the foundation for a risk-on bias—especially across global equities.

Global Equities – Leaning into Global Breadth

Equities remain the favored asset class, supported by lower rates, resilient economic growth, and attractive valuations. These include Asia ex-Japan , with a focus on large-cap cyclicals in Korea, dividend paying state-owned enterprises (SOEs) in China, and growth companies in India.

Europe Still Undervalued with core allocation maintained due to structural reforms and fiscal stimulus, with a focus on: Industrials, Financials, and Technology.

US – Balanced, Not Overexposed remains a core holding, with a focus on: Financials, Technology, Communication Services. Lower USD may cap outperformance versus global peers, but a soft landing and potential Fed cuts support the earnings outlook.

Other Key Asset Classes like Fixed Income, Gold, and Alternatives used to manage volatility.

Risks:

Trade Escalation: A breakdown in tariff negotiations could dampen earnings.

Oil Price Shocks: Geopolitical tensions could cause inflation spikes and policy tightening.

Weak US Hard Data: A sudden economic slip could derail the soft landing narrative.

Strategy in Summary: Capitalize on global equity opportunities, especially in Asia and Europe, while maintaining a diversified core in the US. Use USD weakness as a tailwind—not just for tactical gain, but for strategic rebalancing across asset classes

As the financial world keeps moving, it’s super important to know how your investments are doing. If your portfolio is worth more than $100,000, don’t hesitate! Contact us today at Al Hiary Al-Iktissadi. We’re offering a free look at your portfolio to help you understand your current situation and find smart ways to grow your money. Let’s make your investments work harder for you!